About

In the very competitive world of business, organizations are always looking for methods to set themselves apart from their rivals. The Red Ocean and Blue Ocean strategies are two strategies that have gained popularity recently to compete with rivals.

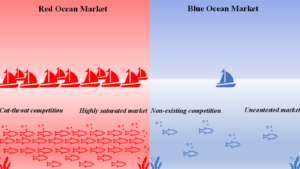

Red Ocean’s strategy concentrates on the current market and strives to beat the competitors. While Blue Ocean’s approach looks to expand into new markets through the introduction of cutting-edge goods and services. Each of these tactics offers a unique way to compete in the market, and they each have advantages and disadvantages. We examine the rationale behind the Red Ocean strategy’s necessity for enterprises in this post.

What is a red-ocean strategy?

The red-ocean strategy is the exact opposite of a blue-ocean plan strategy. It refers to combating an already-existing market when there is little demand and strong competition. A red ocean strategy aims to outperform competitors by providing customers with a value proposition that is comparable to or superior to that of competitors and by enhancing the features, quality, or cost of goods, services, or business models. For example, Burger King and McDonald’s use the Red Ocean strategy to compete with one another in the fast-food market by offering comparable goods and services but with different value propositions. Thus, Red-ocean strategies are frequently linked to effectiveness, efficiency, and optimization.

Benefits and challenges of a red ocean strategy

A company may profit from a red ocean strategy in several ways, including optimizing operational excellence, meeting customer demands, and adjusting to shifting market conditions. But there are drawbacks as well, like being faced with intense competition, losing uniqueness and value, finding it difficult to innovate, and experiencing stress and fatigue. Maximizing operational excellence may streamline systems and processes, cut costs, and minimize waste.

Utilizing current knowledge and capabilities may help build on the company’s and the sector’s strengths and competencies. Meeting or surpassing current customers’ expectations and demands as well as providing continuous quality and service will all contribute to satisfying their wants. To adjust to changes in the market, one must keep an eye on and analyze the movements and patterns of both clients and rivals.

When there is strong competition, there is competition for the same resources and customers as well as pricing and differentiation battles. When competitors become too similar or generic, they can lose their unique selling points and customer loyalty, negatively impacting their profitability.

When you ignore potential opportunities and challenges in the future and place an excessive amount of focus on the market and current products, you may find it difficult to innovate. Dealing with frequent changes and situations of crisis, as well as working under constant pressure and high expectations, can lead to exhaustion and stress.

How to balance innovation and execution in a RED Ocean Strategy

There is no right or wrong answer when it comes to blue ocean and red ocean strategy. The secret is to strike the ideal balance between execution and creativity based on your objectives, available resources, and surrounding circumstances. To do this, begin by identifying the value you wish to produce, who you want to provide it for, and how your strategy will fit into your purpose and values. After that, carry out a competition study to determine market gaps and opportunities as well as your competitors’ advantages and disadvantages. Next, develop a value curve that highlights your unique selling points and highlights the characteristics and advantages of your product or service.

Additionally, implement experiments, surveys, and data collection from stakeholders and customers to verify and test your hypotheses. Lastly, create a business plan and a minimal viable product (MVP), sell your solution to your target market, and evaluate and monitor your key performance indicators.